Latest News

New GDP Series Makes Meeting Fiscal Targets and $4 Trillion Economy Goal More Difficult

Short Overview

India’s revised GDP series has quietly changed the size of the economy on paper. While growth numbers may still look steady, the reduction in nominal GDP makes fiscal deficit targets harder to achieve and complicates India’s ambition of becoming a $4 trillion economy. This blog explains what changed, why it matters, and what it means for India’s economic future.

India’s new GDP series revision has reduced nominal GDP estimates, making fiscal deficit targets and the $4 trillion economy goal harder to achieve. Learn how the revised data impacts fiscal consolidation, debt-to-GDP ratio, nominal growth expectations, and India’s economic roadmap toward 2047 in simple terms.

Table of Contents

- Introduction

- What Changed in the New GDP Series?

- Why Nominal GDP Matters More Than Growth Rates

- Impact on Fiscal Deficit Targets

- The Challenge for FY27 Fiscal Consolidation

- Debt-to-GDP Ratio and Borrowing Pressure

- The $4 Trillion Economy Goal Explained

- Exchange Rate Risks and Global Comparisons

- What This Means for India’s Economic Roadmap

- Conclusion

Introduction

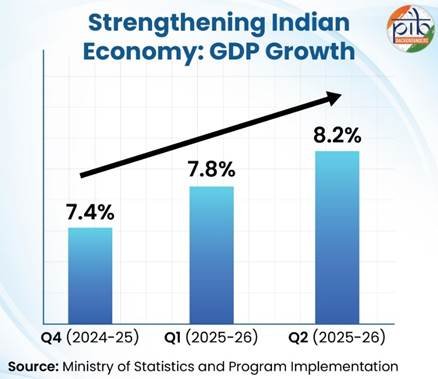

India’s economic data recently went through a major revision. The Ministry of Statistics and Programme Implementation updated the base year for GDP calculations to 2022–23. On the surface, this may sound technical and routine. But the impact is significant.

The new GDP series makes meeting fiscal targets and the $4 trillion economy goal more difficult. While India’s real growth remains strong compared to many global economies, the nominal size of the economy has been revised downward by around 3–4 percent. That change affects fiscal deficit calculations, debt ratios, and even India’s global economic ranking.

To understand why this matters, we need to look beyond headline growth numbers and focus on nominal GDP.

What Changed in the New GDP Series?

When statistical agencies update GDP data, they change the base year to reflect current price structures and better data sources. In this case, the base year shifted to 2022–23.

Under the old series, India’s growth for 2023–24 was estimated at 9.2 percent. Under the new series, it stands at 7.2 percent. However, the more important change is that nominal GDP for 2025–26 has been reduced by about 3.3 percent to ₹345 lakh crore.

This reduction does not mean the economy shrank overnight. It means improved data sources and methods have recalibrated the size of the economy. According to MoSPI officials, such revisions are normal and often smaller as databases improve.

Still, even a 3–4 percent reduction has serious fiscal implications.

Why Nominal GDP Matters More Than Growth Rates

Most people focus on growth rates. But governments operate based on absolute numbers.

Fiscal deficit, debt-to-GDP ratio, and borrowing needs are calculated as percentages of nominal GDP. If nominal GDP becomes smaller, those ratios automatically look larger even if spending remains unchanged.

For example, if the government planned for a 4.4 percent fiscal deficit based on earlier GDP estimates, a lower GDP base pushes that ratio upward. The same spending suddenly appears larger relative to the economy.

That is exactly what is happening now.

Impact on Fiscal Deficit Targets

The Union Budget set the fiscal deficit target for 2025–26 at 4.4 percent of GDP. However, this was based on earlier GDP estimates.

With the revised GDP data lowering nominal output, the fiscal deficit now effectively rises to 4.5 percent for the same year.

Similarly, earlier fiscal deficits have also increased:

The deficit for 2022–23 has moved from 6.5 percent to 6.7 percent.

For 2023–24, it rose from 5.5 percent to 5.7 percent.

For 2024–25, it edged up from 4.8 percent to 4.9 percent.

These may appear like small changes, but in fiscal management, even a 0.2 percent shift can mean thousands of crores in additional borrowing pressure.

The Challenge for FY27 Fiscal Consolidation

The fiscal deficit target for 2026–27 has been fixed at 4.3 percent of GDP, which translates to ₹16.96 lakh crore in absolute terms.

To meet that 4.3 percent target, India now requires nominal GDP growth of 13–14 percent next year. However, the Budget assumption was closer to 10 percent nominal growth.

That gap creates tension.

If nominal growth stays around 10 percent, the fiscal deficit ratio may exceed the target unless the government reduces borrowing or cuts expenditure. Achieving 13–14 percent nominal growth would require strong real growth combined with moderate inflation, which may not be easy in a volatile global environment.

This makes fiscal consolidation more challenging under the new GDP series.

Debt-to-GDP Ratio and Borrowing Pressure

Another important fiscal anchor is the debt-to-GDP ratio.

Earlier estimates suggested that the Centre’s debt-to-GDP ratio would gradually decline. However, with the revised nominal GDP numbers, this ratio is expected to rise.

Estimates suggest it could increase from 56.2 percent to around 58.1 percent in 2025–26. Even with 10 percent nominal growth in 2026–27, the ratio could remain around 57.5 percent, which is higher than the government’s target of 55.6 percent.

A higher debt-to-GDP ratio limits fiscal flexibility. It may lead to higher borrowing costs and restrict public spending on infrastructure, welfare, and development.

This is why the new GDP series makes meeting fiscal targets more difficult in a practical sense.

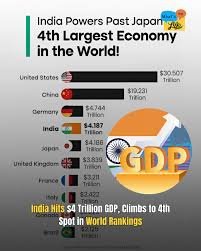

The $4 Trillion Economy Goal Explained

India aims to become a developed nation by 2047. One major milestone in that journey is becoming a $4 trillion economy.

At the current exchange rate of around ₹90.98 per US dollar, India’s GDP in 2025–26 stands at approximately $3.8 trillion.

If nominal GDP grows at 10 percent and the exchange rate remains stable, India could cross the $4 trillion mark next year.

However, there are two important risks.

First, if nominal growth falls short of expectations, the target could be delayed.

Second, exchange rate fluctuations matter significantly. A weaker rupee reduces GDP in dollar terms, even if domestic growth is strong.

Nigeria offers a useful example. Its GDP jumped sharply after rebasing but later declined in dollar terms due to currency depreciation. The same risk applies to India.

Exchange Rate Risks and Global Comparisons

Economic size in dollar terms depends heavily on currency stability.

If the rupee depreciates sharply, India’s GDP measured in dollars shrinks, even if the domestic economy grows steadily.

While capital inflows and trade agreements could support currency stability, global uncertainties, oil prices, and interest rate movements in advanced economies can influence exchange rates.

This makes the $4 trillion economy goal not just a growth challenge but also a currency management issue.

What This Means for India’s Economic Roadmap

The new GDP series does not change the underlying strength of India’s economy. India remains one of the fastest-growing major economies in the world.

However, statistical revisions highlight how tight fiscal planning must be.

To stay on track, India will likely need:

Stronger tax collections driven by compliance and digitalization.

Controlled expenditure growth without compromising capital investment.

Sustained real GDP growth above 7 percent.

Stable inflation to support nominal growth.

Exchange rate stability to maintain dollar valuation.

The path to fiscal consolidation is now narrower, but not impossible.

Conclusion

The new GDP series makes meeting fiscal targets and the $4 trillion economy goal more difficult, but not unattainable.

The revision has reduced nominal GDP estimates, which in turn increases fiscal deficit ratios and debt-to-GDP numbers. This means India must now achieve higher nominal growth or recalibrate borrowing to stay within fiscal limits.

While growth fundamentals remain strong, the challenge ahead is about discipline, stability, and smart policy execution.

India’s long-term goal of becoming a developed nation by 2047 remains intact. However, the journey will require tighter fiscal management and sustained economic momentum under the revised statistical framework.

New GDP Series Makes Meeting Fiscal Targets and $4 Trillion Economy Goal More Difficult

BMRCL Deploys Eighth Trainset on Namma Metro Yellow Line: What It Means for Bengaluru Commuters

Indian Airlines Halt West Asia Flights After Israel-US Attack on Iran Triggers Major Airspace Shutdown

India GDP Growth 7.6% in FY26: New GDP Series Upgrades Growth but Lowers Economy Size

India Missing Out on Big Agriculture Export Opportunity: Path to $100 Billion by 2030

ಮ್ಯೂಚುವಲ್ ಫಂಡ್ SIP ಮೂಲಕ 15 ವರ್ಷಗಳಲ್ಲಿ ₹10 ಕೋಟಿ ರೂಪಾಯಿ ಗಳಿಸುವುದು ಹೇಗೆ?

Aadhar Model Smart Card To Farmers: ರೈತರಿಗೆ ಆಧಾರ್ ಮಾದರಿ ಸ್ಮಾರ್ಟ್ ಕಾರ್ಡ್ ಯೋಜನೆ – ಸಂಪೂರ್ಣ ಮಾಹಿತಿ, ಅನುಕೂಲತೆಗಳು ಮತ್ತು ನೋಂದಣಿ ವಿವರಗಳು

ಕೇಂದ್ರ ಬಜೆಟ್ 2026 ಕೃಷಿಕರಿಗೆ ಏನು ಕೊಡುಗೆ? ಭಾರತ್ ವಿಸ್ತಾರ್ AI ಪರಿಕರದಿಂದ ರೈತರಿಗೇನು ಲಾಭ?

Farming: ಹಳ್ಳಿಗಳಿಗೆ ಹಿಂದಿರುಗಿ ಕೃಷಿಯತ್ತ ಒಲವು ತೋರುತ್ತಿರುವ ವೃತ್ತಿಪರರು – ನಿಜವಾದ ಕಾರಣಗಳು ಮತ್ತು ಭವಿಷ್ಯದ ಜೀವನಶೈಲಿ

What Is the Best Climate for Saffron Cultivation?

Union Budget 2026–27 Agriculture Initiatives: Transforming Indian Farming for Global Markets

What Are the Best Mushrooms to Grow for Profit?

Budget 2026 Agriculture Policy: Push for High-Value Crops but Farmers Still Struggle

ಭಾರತದಲ್ಲಿ ಮಣ್ಣಿನ ಆರೋಗ್ಯ: ಸುಸ್ಥಿರ ಕೃಷಿ ಮತ್ತು ಆಹಾರ ಭದ್ರತೆಗೆ ಅಡಿಪಾಯ

2025ರ ವಾಣಿಜ್ಯ ಧಾನ್ಯ ಕೃಷಿಯ ಹೊಸ ಆವಿಷ್ಕಾರಗಳು: ಸ್ಮಾರ್ಟ್ ನೀರಾವರಿ, ಗೊಬ್ಬರ ಮತ್ತು ಪ್ರೆಸಿಷನ್ ಸ್ಪ್ರೇಯರ್ಗಳು

How to Start Kesari (Saffron) Farming in India?

ಕೇಸರಿ (Saffron) ಬೆಳೆಯಲು ಅತ್ಯುತ್ತಮ ಹವಾಮಾನ ಯಾವುದು?

ಕೇಸರಿ ಕೃಷಿಗೆ ಎಷ್ಟು ಹೂಡಿಕೆ ಅಗತ್ಯವಿದೆ?

ಕಬ್ಬು ಬೆಳೆಯಲು ಸೂಕ್ತ ಸಲಹೆಗಳು – ಹೆಚ್ಚಿನ ಇಳುವರಿ ಮತ್ತು ಲಾಭಕ್ಕಾಗಿ ಸಂಪೂರ್ಣ ಮಾರ್ಗದರ್ಶಿ